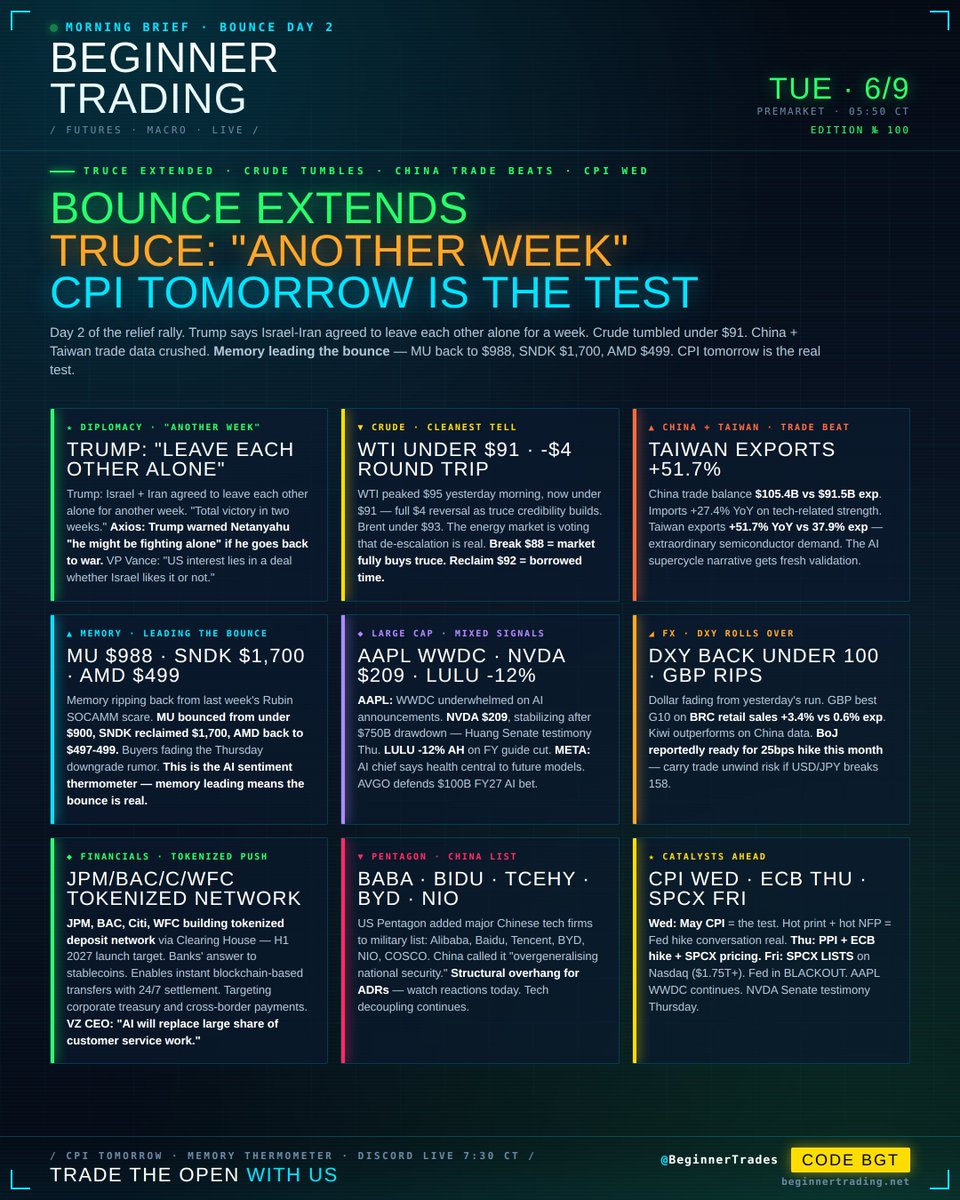

🌅 Morning Market Brief — Tuesday, June 9, 2026

Risk-on continues. Trump says Israel and Iran agreed to "leave each other alone for another week." Crude tumbled overnight. China trade data crushed. Memory stocks attempting to bounce. CPI tomorrow remains the real test.

📊 Where The Tape Is

NQ futures: 29,657 — up from yesterday's 29,435 close (+222 / +0.75%)

ES futures: 7,447 — up from yesterday's 7,412.25 close (+34.75 / +0.47%)

GC (Gold): $4,355 — basically flat, holding above 200-day MA

CL (Crude): WTI ~$89-91 range — softer continuing yesterday's afternoon selloff

BTC: $62,655 — slightly softer, trading either side of $63K

Read: The bounce extends. Two-day relief rally with geopolitical risk dialing back. But notice the deceleration — yesterday NQ gapped up 1.6% from Friday close, today's adding another 0.75% but at a slower pace. Markets getting cautious into CPI.

🕊️ Trump Says Israel/Iran Agreed To "Another Week" Truce

Major shift in tone from yesterday:

Trump's statements:

"Israel and Iran agreed to leave each other alone for another week"

"We are negotiating with Iran, a victory will happen very soon"

"Will declare total victory in two weeks"

"Oil prices will come down post-Iran"

"Could have an idea on an Iran deal in one or two days"

Per Axios (late Monday): In a call with Netanyahu, Trump warned that "if the Israeli leader went back to war with Iran, he might be fighting alone." That's the clearest US-Israel daylight signal we've seen.

VP JD Vance jumped in:

"Potential Iran deal will be a home run for the American people"

"The US's interest lies in a deal with Iran, whether Israel likes it or not"

"Primary goal is to prevent Iran from acquiring a nuclear weapon"

The honest caveats:

A top Iranian official told CNN a deal is "doubtful due to persistent major roadblocks regarding nuclear program and uranium enrichment"

Iranian official to Al Jazeera: "No agreement unless frozen funds released and sanctions lifted"

Iran's UN envoy: hopes for talks conclusion by end of June, exchanging views via Pakistan

Two Israeli airstrikes overnight on southern Lebanon (Tyre) — so it's not a full truce yet

Houthi warning: A military source said the Houthis are "preparing major military surprises" with "high quality" weapons for naval/aerial conflict. Even if Israel-Iran cools, the Red Sea situation isn't done.

💾 Memory Sector — Attempting To Stabilize After Brutal Week

Updated Memory Picture (Verified)

$MU: $988 — bouncing back from under $900 last week. Roughly +10% from the lows

$SNDK : $1,700 — hit that level this morning. Reclaiming territory it lost Thursday-Friday

$AMD : $497-499 — back near the highs after the recent dip

$NVDA: $209 — still working off the $750B+ market cap loss but stabilizing

The reframe: Memory IS leading the bounce, not lagging it. That's actually a BIG bullish signal — the Thursday Rubin SOCAMM downgrade rumor is getting faded by buyers willing to step in at the lows. If the rumor were fundamentally true, MU wouldn't be reclaiming $988 this fast.

What triggered Thursday's crash: A market rumor that NVIDIA's next-generation Rubin platform will reduce SOCAMM memory capacity from 55TB per rack down to 28TB per rack. That implies far less DRAM/memory demand per AI server than previously priced in — and memory has been the strongest theme in semis all year.

The bull counter-narrative emerging:

NVIDIA officially announced HBM4 partnership with SK Hynix for the Vera Rubin platform — Jensen confirmed Samsung, Hynix, and MICRON all qualified to supply HBM4

Jensen Huang weekend: "AI revolution just beginning, chip plunge is a buying opportunity"

Taiwan exports +51.7% YoY — strongest semiconductor demand signal in years

China imports +27.4% YoY — tech-related imports leading

What to watch on memory today:

HBM4 vs SOCAMM are different products. HBM4 sits directly on the GPU (high-end, high-margin). SOCAMM is the CPU-side memory that allegedly got downgraded. MU and SNDK are exposed to BOTH.

If MU can reclaim $920-940, the Thursday drop becomes a "look-back" buy opportunity

If $MU breaks $880, the next leg lower starts

The bigger picture: Memory is the highest-beta way to play AI infrastructure. When NVDA goes up 3%, MU goes up 5%. When NVDA goes down 3%, MU goes down 8%. The Rubin rumor introduced structural uncertainty into a previously airtight bull case.

📈 Large Cap Stock News Worth Knowing

Apple $AAPL — WWDC Day 2:

Yesterday's keynote underwhelmed Wall Street on AI announcements

New iOS features focused on incremental productivity tools, not the AI step-change traders wanted

Stock barely budged after the event — bearish signal in itself

Foldable iPhone speculation continues per Nippon Electric Glass partnership news

NVIDIA $NVDA — $209, Still Heavy:

Shed over $750B from June peak

HBM4 partnership news helped but didn't reverse

Jensen Huang testifying before Senate Banking Committee June 11 — Sen. Warren's questioning on China sales is the wild card

US officials reportedly debating whether May 2025 export controls created loopholes for Chinese firms to buy Blackwell chips abroad

Alphabet $GOOGL:

Google Cloud cutting staff in Threat Intelligence Group, Mandiant, and other cloud teams

Citing "reinvestment in AI growth areas"

Combined with last week's -4% on $80B raise = sentiment shift on GOOGL

Meta $META:

AI chief Alexandr Wang said health will be central to future AI models and could differentiate consumer offerings

Muse Spark health capabilities cited as strength but "remains behind leading frontier models"

Decided NOT to make Muse Spark open source due to biological-risk concerns

Broadcom $AVGO :

CEO Hock Tan defending the Thursday wreck: "AI infrastructure demand is almost insatiable"

Says less focused on acquisitions now because AI offers stronger organic growth

Expects Broadcom's AI business to generate $100B+ in FY 2027

Stock still down ~13% from Thursday print

Tesla $TSLA:

Exported 38.7K China-made vehicles in May per CPCA

China passenger vehicle sales -22.3% Y/Y in May — broader market weakness

TSLA on Pentagon's broader Chinese tech radar via supply chain exposure

Verizon $VZ:

CEO: "AI will replace a large share of customer service work"

$20M set aside to retrain workers for AI-related roles

7,000 employees already applied

First positive Q1 phone subscriber additions since 2013 reported in April

JPMorgan, BAC, Citi, Wells Fargo:

Building a tokenized deposit network through the Clearing House

Target: H1 2027 launch

Enables instant blockchain-based transfers with 24/7 settlement

Targeting corporate treasury, liquidity management, cross-border payments

This is the banks' answer to stablecoins

Lululemon $LULU :

Slumped 11.7% Monday after-hours on FY guidance cut

Cited "negative brand commentary, underwhelming product launches, weak North America"

FY EPS now seen 10.95-11.15 (was 12.10-12.30, consensus was 12.27)

Americas comps -5%, international +13% — bifurcated brand story

🛢️ Crude — The Cleanest Tell

Oil is selling off hard — strongest market validation that the ceasefire is being believed:

WTI Jul: $88.80-$91.55 range — down from yesterday's $94.61 surge

Brent Aug: $92.00-$94.42 range — Brent -1.5% on the session

The full move: WTI peaked near $95 yesterday morning, now under $91 — a $4+ round-trip

The Vance comment matters: When the VP openly says the US will pursue a deal "whether Israel likes it or not," oil traders take that as serious de-escalation signaling.

🇨🇳 Chinese Trade Data — Huge Beat

China dropped one of the strongest trade prints in years:

Trade Balance: $105.4B vs $91.5B expected (vs $84.8B prior)

Exports: +19.4% YoY vs +14.3% expected

Imports: +27.4% YoY vs +25% expected — robust tech-related imports

Taiwan also reported huge:

Exports: +51.7% YoY vs +37.9% expected — extraordinary semiconductor demand signal

Imports: +54.9% YoY vs +37.4% expected

The catch: US Pentagon added Chinese military companies to its list, including Alibaba, Baidu, BYD, Tencent, NIO, and Cosco. China condemned it as "overgeneralising national security." Structural overhang.

US also asked China to resume rare earth exports to Japan — Washington concerned about global high-tech supply chains.

💵 Bonds & Currencies

Dollar rolling over slightly:

$DXY back below 100.00 — fell back from yesterday's run

99.80 was Monday's support, 100.00 is where DXY typically loses steam

Pound (GBP) leading G10:

BRC retail sales beat huge — +3.4% YoY vs 0.6% expected (from -3.4% prior)

UK consumer remarkably resilient despite Iran situation

Kiwi outperforming on Chinese trade data strength

Yields:

USTs slightly firmer (2 ticks)

Lower energy prices easing pressure on bonds

CPI tomorrow + PPI Thursday are the real catalysts

🏦 BoJ Reportedly Prepared To Hike 25bps This Month

Major central bank news from Nikkei:

BoJ prepared to raise rates by 25bps at its June meeting

Hike preparing for risk of upward revision of inflation

Will begin discussions on discontinuing quarterly reduction in government bond purchases from April 2027

Market implication: This is the carry trade unwinder. If BoJ hikes while others pause/cut, USD/JPY pressure intensifies.

₿ bitcoin:native Trades Either Side Of $63K

Currently $62,655 — slightly softer

Steady around the $63K handle as the token consolidates

Last week's $60,880 Saturday low holding as the floor

ETH still pressured at 1-year lows

The picture: BTC isn't rallying on the Iran de-escalation. Crypto-specific headwinds (ETF outflows, MSTR sale, Mt. Gox supply) matter more than macro right now.

🎯 The Trade Setup For Today

The asymmetry: Markets pricing in successful Iran de-escalation. If anything breaks that narrative (Israel breaks the "week," Iran rejects MoU draft, Houthi "surprise") — we re-test Friday's lows fast.

Three things to watch:

Crude continuation — WTI breaks $88 = market fully bought the truce. Reclaims $92 = bounce on borrowed time.

CPI positioning into tomorrow — yields holding 4.50%+ keeps tech multiple-compression risk alive. Hot CPI tomorrow + hot NFP from Friday = Fed hike conversation gets very real.

Memory stocks $MU, $SNDK — these are your AI sentiment thermometer. If memory leads the bounce today, the dip-buying is real. If memory stays heavy while NQ rallies, the rally has weak foundation.

🎓 Educational Note Of The Day

Why "first hour reversals" happen so often after big gap moves

When markets gap up significantly at the open (like NQ +1.6% yesterday), the first hour of cash trading frequently sees a reversal or significant pullback. Here's why:

1. Overnight gaps come from futures, not real volume.A gap up of 200+ NQ points is built on relatively thin overnight liquidity. When New York opens at 9:30 AM ET, you suddenly have institutional desks, ETF rebalancing, options market makers, and retail flow ALL hitting the tape at once. The thin gap meets thick volume — and the gap often gets challenged.

2. Gap fade is a real strategy.There are entire institutional desks built around fading opening gaps. The data supports them: roughly 60-65% of gap-ups above 1% see at least a partial fill in the first 60 minutes of cash trading.

3. Overnight news has time to be re-evaluated. At 5 AM CT, you reacted to Trump's tweet emotionally. By 9 AM, smarter desks have read the fine print, considered Iran's official response, checked oil's behavior, and decided whether to chase or fade. That reassessment process IS the morning reversal.

The trading framework:

Strong gap + strong volume on the open + holds above pre-market high in first 5 minutes = trend day up, lean long

Strong gap + weak volume on the open + immediately rejects pre-market high = fade likely, lean short the bounce

Strong gap + chop in first 15 minutes = wait, no edge

The lesson from yesterday's tape: the bounce held into the close, which means today's gap-up at 9:30 is starting from a stronger foundation than yesterday's was. Yesterday was a coin-flip reversal risk. Today the trend bias is stronger.