비트코인 5만 달러 아래로 떨어질 확률 거의 없음

0

91

0

06-05

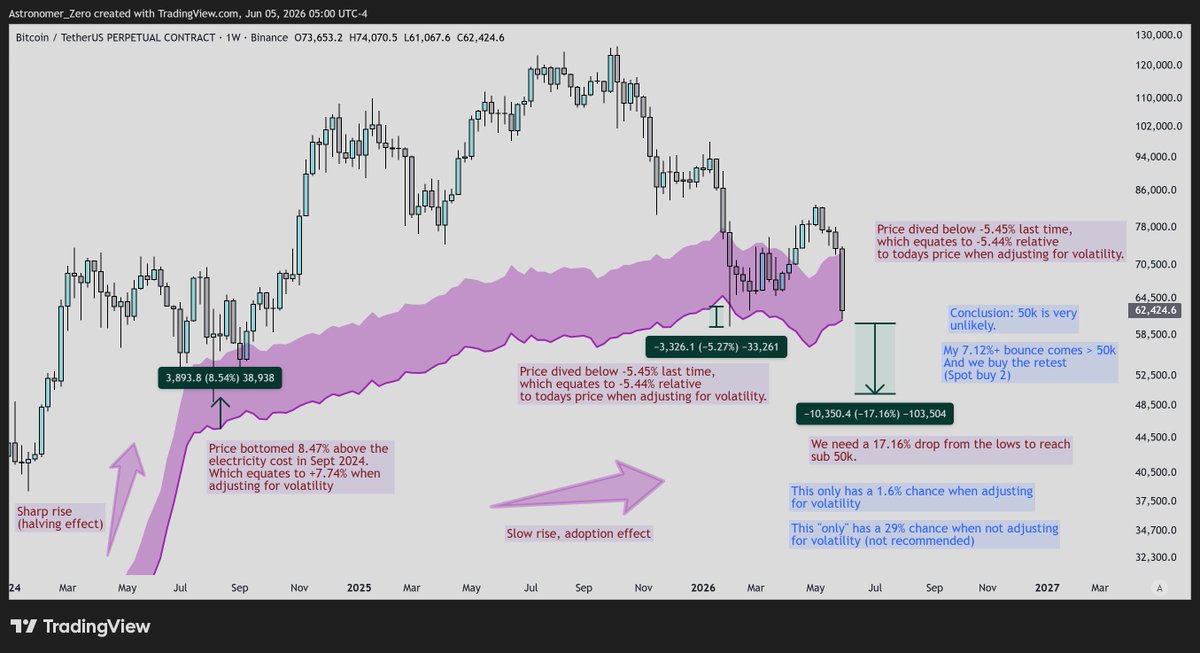

비트코인 변동성 조정 기준으로 5만 달러 밑으로 내려갈 확률이 98.4% 아니라고 봄. 이전에 채굴 전기료 지표로 바닥 찍었다고 했는데, 그때 6만에서 8.3만까지 37% 급등한 거 실시간으로 맞춤. 이 신호가 워낙 중요해서 좀 더 깊게 분석해봄. 여기저기서 막 숫자 던지고, 약세장 예상하며 5만 이하 간다고 자랑하는 사람들 많은데, 지금 필요한 건 최소한 하나라도 확실한 지표랑 데이터임. 좋은 데이터는 논쟁하기 힘든 법인데, 물론 해석은 사람마다 다를 수 있음. 근데 이건 해석 폭이 좁아서 데이터 분석할 때 딱 맞는 사례임. 고등학교 통계 배운 사람은 알겠지만, 3번 100% 확률 나왔다고 4번째도 무조건 그런 건 아님. 그래서 이번 글은 강력한 데이터랑 그 데이터가 왜 그런지 설명해서 그냥 데이터만 던지는 블랙박스 효과 없애려고 함. 채굴자 1비트코인 생산 전기료가 핵심 지표임. 채굴자 영향력 논란 많지만, 반감기 이후 연간 0.84% 비트코인 인플레(약 16만 4천 BTC)가 있음. 지금 비트코인 가격 6.1만 달러 기준으로 연간 107억 달러 규모임. 매년 마이크로스트래티지 보유량 6분의 1이 채굴자 손에 들어가는데, 비트코인 유동성 얇은 상황에서 이걸 시장에 쏟아내면 안 좋음. 채굴자 영향력은 여전히 매우 중요함.

0개의 댓글

| No | 제목 | 닉네임 | 조회수 | 추천 | 등록일 |

|---|---|---|---|---|---|

| 제목 | |||||

| 7668 | 0 | 0 | 07-20 17:56 | ||

| 7667 | 0 | 0 | 07-20 22:20 | ||

| 7666 | 0 | 0 | 07-20 22:50 | ||

| 7665 | 0 | 0 | 07-20 23:00 | ||

| 7664 | 0 | 0 | 07-20 23:01 | ||

| 7663 | 0 | 0 | 07-20 23:25 | ||

| 7662 | 0 | 0 | 07-20 23:40 | ||

| 7661 | 0 | 0 | 07-20 23:46 | ||

| 7660 | 0 | 0 | 07-20 23:48 | ||

| 7659 | 0 | 0 | 07-20 20:08 | ||

| 7658 | 0 | 0 | 07-20 20:26 | ||

| 7657 | 0 | 0 | 07-20 21:06 | ||

| 7656 | 0 | 0 | 07-20 21:09 | ||

| 7655 | 0 | 0 | 07-20 21:30 | ||

| 7654 | 0 | 0 | 07-20 21:33 | ||

| 7653 | 0 | 0 | 07-20 22:02 | ||

| 7652 | 0 | 0 | 07-20 21:02 | ||

| 7651 | 1 | 0 | 07-20 18:59 | ||

| 7650 | 1 | 0 | 07-20 19:25 | ||

| 7649 | 2 | 0 | 07-20 06:11 | ||

$CRCL 300달러는 쉽지 않아 보임

|

|||||

비트코인 바닥 신호 감지돼서 #MomentumMonday 확장함

|

|||||

인프라 좋아지고 규제 명확해지면 리테일 랠리 가능성 있음

|

|||||

비트코인 올해 바닥 찍은 듯

|

|||||

알트코인 시즌 시작됐나?

|

|||||

이더리움 $7,000 전 마지막 함정 세팅 중

|

|||||

이더리움 2,000 먼저 찍고 최종 하락 올 듯

|

|||||

마지막 급락 기다리는 사람 많음

|

|||||

비트코인 펀딩 점점 약세장 분위기

|

|||||

비트코인 바닥 10월설은 틀렸음

|

|||||

비트코인 EMA50 저항 맞고 6.5만 달러선 붕괴

|

|||||

AI 관련 강세장과 약세장 갈림길인 듯

|

|||||

스트래티지 달러 보유 32억 달러로 늘림

|

|||||

PUMP 코인 강세장 대비 스트래티지 총정리

|

|||||

8월 중순부터 스케일링 시작 예정

|

|||||

BTC 대규모 플래시 크래시 임박

|

|||||

스트래티지, 달러 보유고 2억 2,500만 달러 증가

|

|||||

이번 주 시장 변동성 주의

|

|||||

비트코인 5주 만에 최고 주봉 마감

|

|||||

카스파는 비트코인과 다른 자체 사이클 가짐

|